Love is the most uncensored emotion that creeps unknowingly in each of our lives. Or, to put it better, it has been ubiquitously present as a part of our existence. Underlying in almost every benevolent act of ours, we celebrate it every day. But just as a sapien needs his birthday to claim another year to their existence, we have Valentine’s Day celebrated each year as the day of love. St. Valentine would feel alien to the concept of an entire week of roses, hugs, kisses, teddy bears and chocolates but Valentine’s Day has actually become a fairly commercial, multi-million industry on the rise each year.

In this second post of our 3-part Valentine’s series – #MattersOfHeartAndWallet, we explore how India shops, and splurges, on Valentine’s week.

Love is not a commodity to be bought or sold, of course, but today love has equal sync with money and romance. India has seen a steep surge in Valentine’s Day rush in terms of gifts, dates, and trips whether for partner or others, whether as a couple or all alone. Let us mark in terms of numbers the trends in India of how love transpires and conspires to empty our kitties.

Indians Love Valentine Gifting

We like to pamper each other when in love and what better day than Valentine’s’ Day to do that. The spending stats of Indians show some interesting and some queer facts about the expenditure on love:

A survey by CashKaro.com indicated that about three-quarters of couples bought gifts for their partners to celebrate the Day, while 80% thought this was essential practice for Valentine’s Day.

Younger couples lead the way here – those indulging their partners through gifts most commonly belonged to the age group of 16-24 years. India, with 70% of its population below the age of 35 years, is sure to witness a rapid increase in this gifting trend in the coming years. Interestingly, 77% of the men felt that they ought to pay on dates.

The Heart & Wallet Go Hand In Hand

Valentine’s Day records the third-highest number of orders (after Diwali and Raksha Bandhan) placed for gifts in India. Money and love have surely got a connection with each other when it comes to 14th February. Thousands of crores are spent on gifts and dates all across the lovestruck regions of India. Take a look at the facts:

- Even as early as 2014, we’d seen a whopping INR 16,000 crores being spent, which swelled to 22,000 crores next year.

- A majority of the people spent anywhere between

INR 1500 – 3000 on flowers, candies, and chocolates among other gifts. - Corporate employees and those aged 30+ years prefer more expensive gifts, with their spendings ranging anywhere between INR 1000 – 50,000. For the younger generation, the range comes down to INR 500 – 10,000.

- Another interesting finding is – changing gender roles. Women between 25-35 years spend 35% more than their male counterparts.

V-Day Preferences

When it comes to making our loved ones happy, we don’t count the bills. The week starts with Rose Day, when gifting flowers especially roses and orchids are the trends, followed by other days such as Chocolate Day, Teddy Day and others before Valentine’s Day finally arrives. Besides gifts, people like to go for dates, on holidays and on short adventure trips as well. Check out the trends:

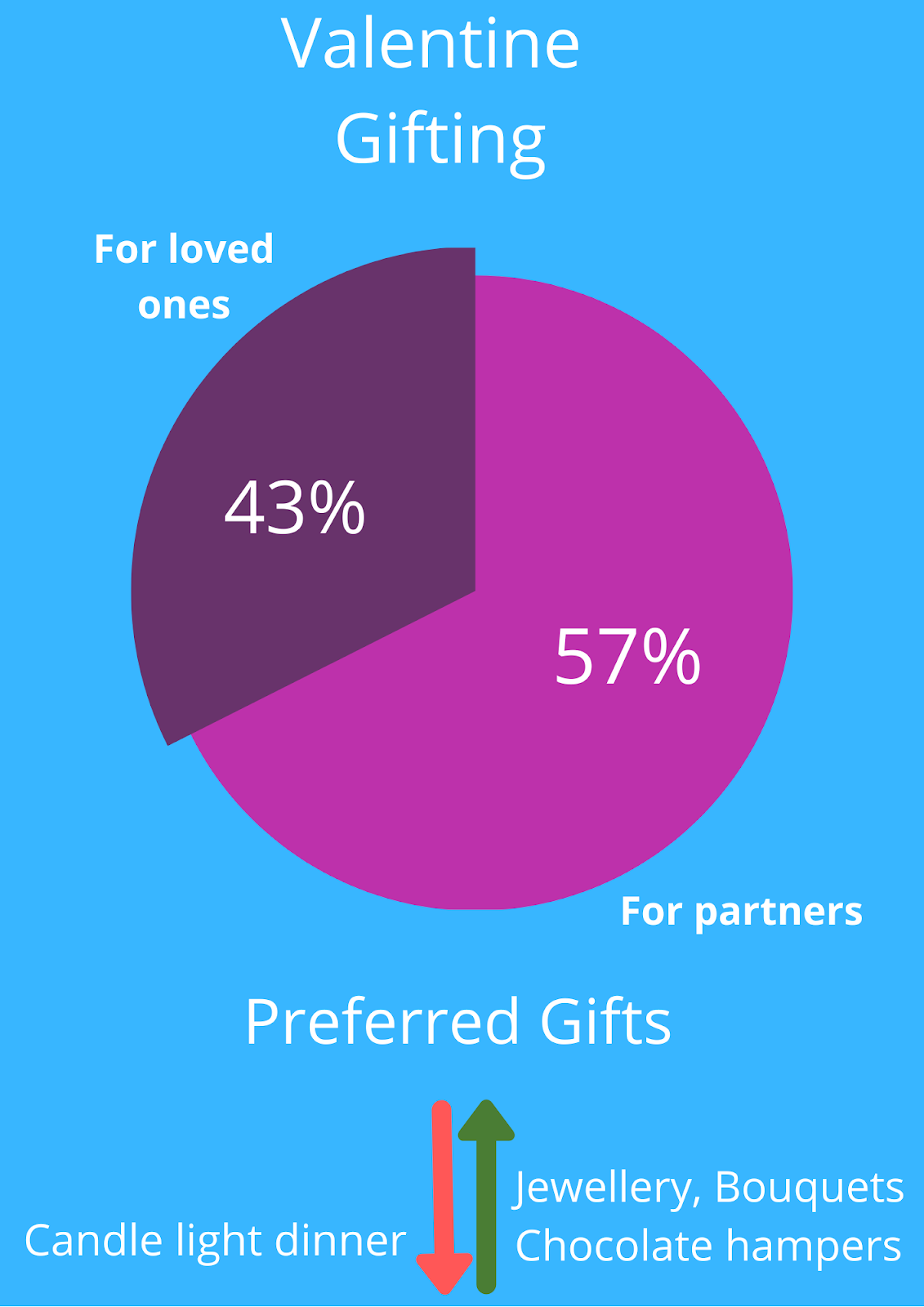

- Candlelight dinners seem to be losing their popularity. The top preferred gifts now are Jewellery, Bouquets, Chocolate hampers, and Teddy Bears.

- People don’t just gift their partners. About 43% of the gift orders placed were for loved ones other than the buyer’s partner.

- We’re also opting for more thrilling options too – such as adventure sports like bungee jumping, surfing, among others, and holidays to offbeat destinations.

- Singles are trying to find love in pampering themselves. The number of trips by solo-travelers to foreign locations increases considerably around Valentine’s Day.

This V-Day why to worry about managing your finances

Indians are die-hard romantics and know how and when to please their loved ones. But sometimes these splurging can fall heavy on the pockets of the salaried class. Enjoy each moment of this Valentine’s Day and shower your partner with gifts and dates without the worry of managing your finances. With Fibe, you can get an instant loan from anywhere between INR 2,000 to INR 2,00,000 at rates of interest as low as Rs 9/day. The loan amount can be availed of even if the employee has no credit ratings. The loan amount can be paid in installments over a period of time adjustable as per your needs and convenience.

So don’t stop yourself from proposing your crush or rekindling your romance this Valentine’s.